Example of Lecture 14, 15 – ARIMA for time series#

Example from: https://www.projectpro.io/article/how-to-build-arima-model-in-python/544

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from time import time

import datetime

from sklearn.ensemble import RandomForestRegressor as RFR

from sklearn.linear_model import LinearRegression as LinearR

from sklearn.model_selection import KFold, cross_val_score as CVS, train_test_split as TTS

from sklearn.metrics import mean_squared_error as MSE

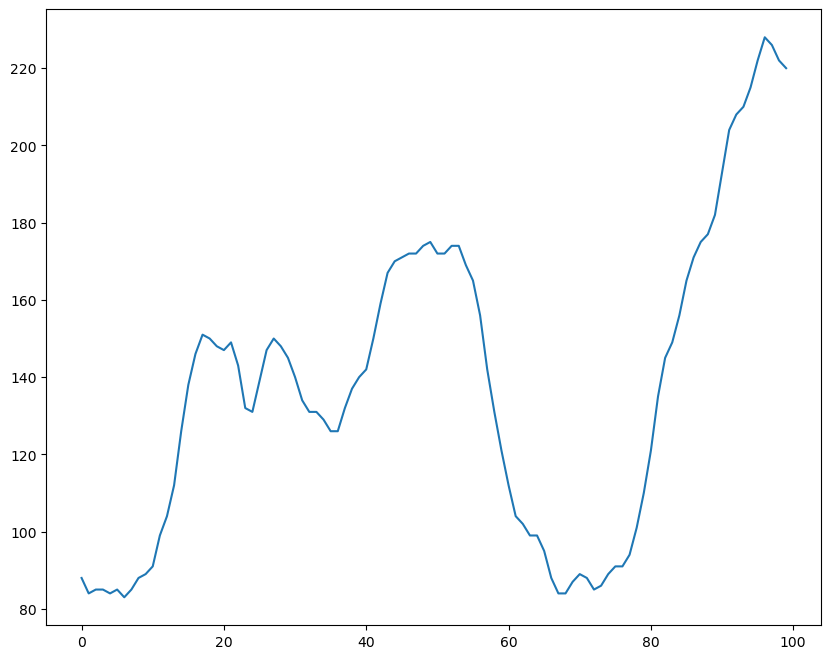

df = pd.read_csv('WWWusage.csv', names = ['index','time','value'], header = 0)

print(f"Total samples are: {len(df)}")

fig = plt.figure(figsize = (10, 8))

ax = fig.add_subplot(1,1,1)

ax.plot(df['value'])

plt.show()

Total samples are: 100

ARIMA(p,d,q)#

p: order of autocorrection

d: order of differential

q: order of moving average

The key to build a ARIMA model is to choose proper p, d, q

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

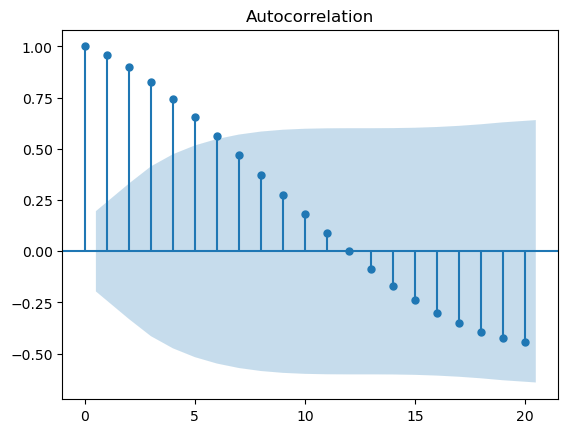

plot_acf(df.value)

plt.show()

Clearly, the data is not ideal for the ARIMA model to directly start autoregressive training. So let’s see how the differencing segment of ARIMA makes the data stationary.

f = plt.figure(figsize = (12, 5))

ax1 = f.add_subplot(121)

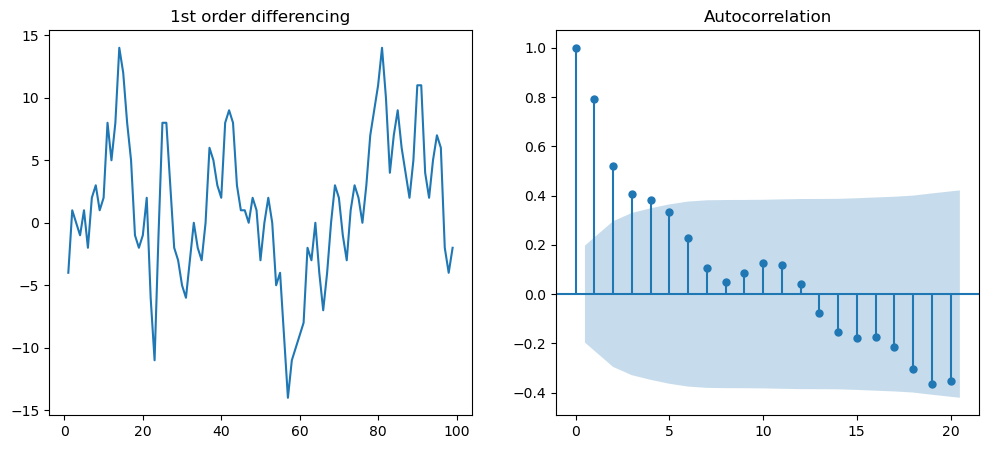

ax1.set_title("1st order differencing")

ax1.plot(df.value.diff())

ax2 = f.add_subplot(122)

plot_acf(df.value.diff().dropna(),ax=ax2)

plt.show()

As seen above, first-order differencing shakes up autocorrelation considerably. We can also try 2nd order differencing to enhance the stationary nature.

# In the following, we will do for second differencing

f = plt.figure(figsize = (12, 5))

ax1 = f.add_subplot(121)

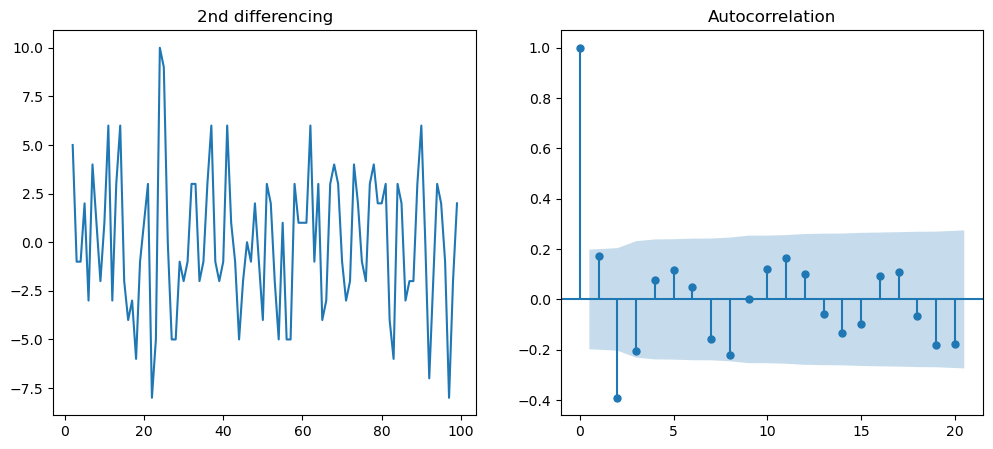

ax1.set_title('2nd differencing')

ax1.plot(df.value.diff().diff())

ax2 = f.add_subplot(122)

plot_acf(df.value.diff().diff().dropna(),ax=ax2)

plt.show()

# Non stationary test by ADF test

from statsmodels.tsa.stattools import adfuller

result = adfuller(df.value.dropna())

print('p-value: ', result[1])

result = adfuller(df.value.diff().dropna())

print('p-value: ', result[1])

result = adfuller(df.value.diff().diff().dropna())

print('p-value: ', result[1])

p-value: 0.12441935447109487

p-value: 0.07026846015272728

p-value: 2.843428755547158e-17

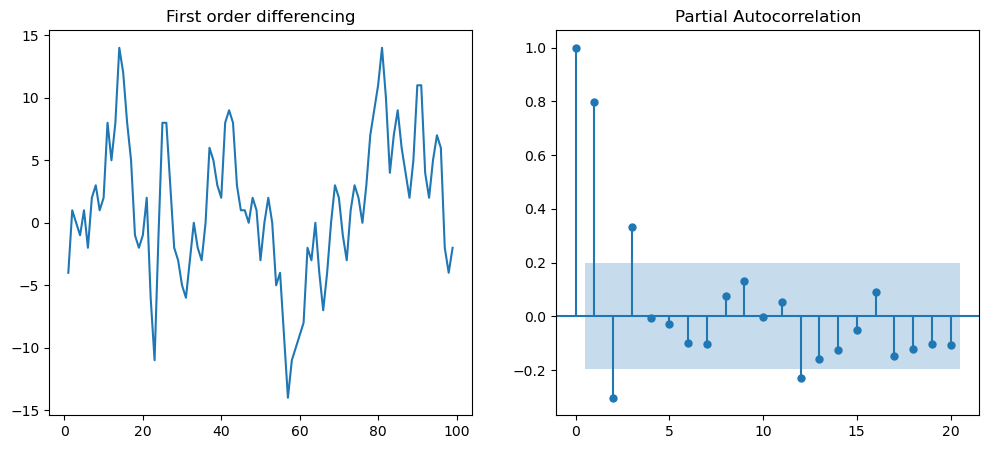

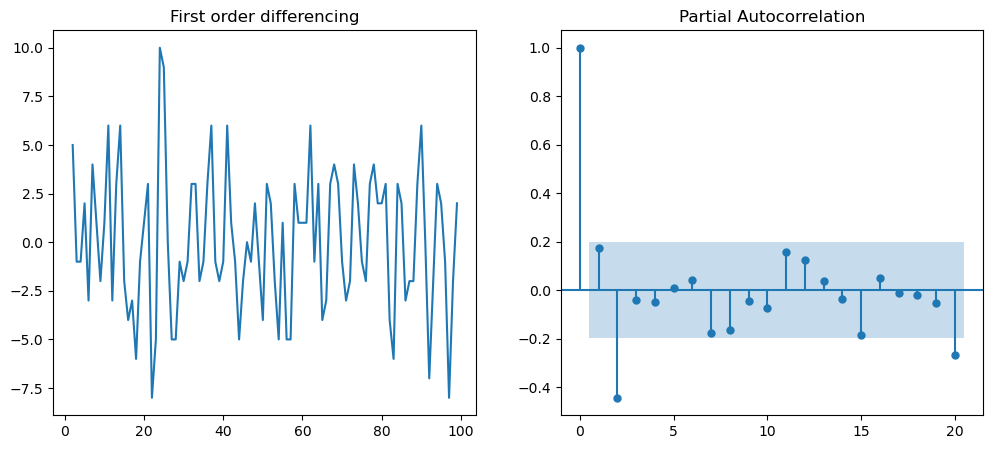

# Next we can determine the value of "p" for first differencing

f = plt.figure(figsize=(12,5))

ax1 = f.add_subplot(121)

ax1.set_title('First order differencing')

ax1.plot(df.value.diff().dropna())

ax2 = f.add_subplot(122)

plot_pacf(df.value.diff().dropna(), ax=ax2)

plt.show()

# Next we can determine the value of "p" for second differencing

f = plt.figure(figsize=(12,5))

ax1 = f.add_subplot(121)

ax1.set_title('First order differencing')

ax1.plot(df.value.diff().diff().dropna())

ax2 = f.add_subplot(122)

plot_pacf(df.value.diff().diff().dropna(), ax=ax2)

plt.show()

Thus, final ARIMA model defined as ARIMA(p=1, d=1,q= 2).#

PART II: Fit the ARIMA model#

from statsmodels.tsa.arima.model import ARIMA

arima_model = ARIMA(df.value, order = (1,1,2))

model = arima_model.fit()

print(model.summary())

SARIMAX Results

==============================================================================

Dep. Variable: value No. Observations: 100

Model: ARIMA(1, 1, 2) Log Likelihood -254.126

Date: Fri, 20 Jan 2023 AIC 516.253

Time: 18:47:18 BIC 526.633

Sample: 0 HQIC 520.453

- 100

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.6976 0.130 5.365 0.000 0.443 0.952

ma.L1 0.4551 0.169 2.699 0.007 0.125 0.786

ma.L2 -0.0664 0.157 -0.424 0.671 -0.373 0.241

sigma2 9.7898 1.421 6.889 0.000 7.005 12.575

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 0.09

Prob(Q): 0.98 Prob(JB): 0.95

Heteroskedasticity (H): 0.63 Skew: -0.07

Prob(H) (two-sided): 0.19 Kurtosis: 3.03

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

# test another setting of (p, d,q)

arima_model = ARIMA(df.value, order = (1,2,2))

model = arima_model.fit()

print(model.summary())

SARIMAX Results

==============================================================================

Dep. Variable: value No. Observations: 100

Model: ARIMA(1, 2, 2) Log Likelihood -252.594

Date: Fri, 20 Jan 2023 AIC 513.189

Time: 18:48:28 BIC 523.529

Sample: 0 HQIC 517.371

- 100

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.6530 0.103 6.359 0.000 0.452 0.854

ma.L1 -0.4743 2.191 -0.217 0.829 -4.768 3.819

ma.L2 -0.5251 1.130 -0.465 0.642 -2.740 1.689

sigma2 9.8299 21.283 0.462 0.644 -31.884 51.544

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 0.22

Prob(Q): 0.95 Prob(JB): 0.90

Heteroskedasticity (H): 0.61 Skew: -0.11

Prob(H) (two-sided): 0.16 Kurtosis: 3.08

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

model.plot_predict(dynamic=False)

plt.show()

---------------------------------------------------------------------------

AttributeError Traceback (most recent call last)

~\AppData\Local\Temp\ipykernel_26020\2666529794.py in <cell line: 1>()

----> 1 model.plot_predict(dynamic=False)

2 plt.show()

~\Anaconda3\lib\site-packages\statsmodels\base\wrapper.py in __getattribute__(self, attr)

32 pass

33

---> 34 obj = getattr(results, attr)

35 data = results.model.data

36 how = self._wrap_attrs.get(attr)

AttributeError: 'ARIMAResults' object has no attribute 'plot_predict'

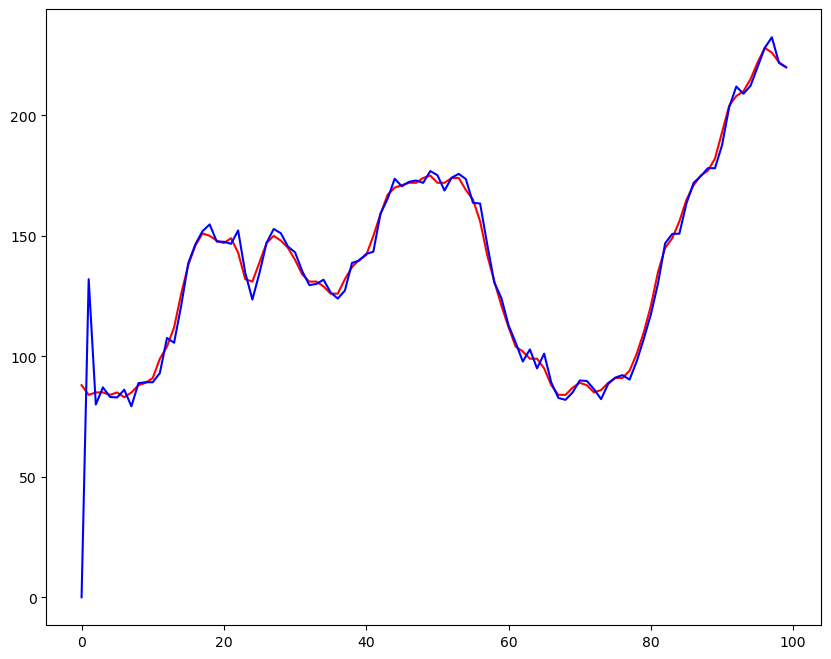

plt.figure(figsize = (10,8))

plt.plot(df.value, color = 'r')

plt.plot(model.predict(),color = 'b')

plt.show()

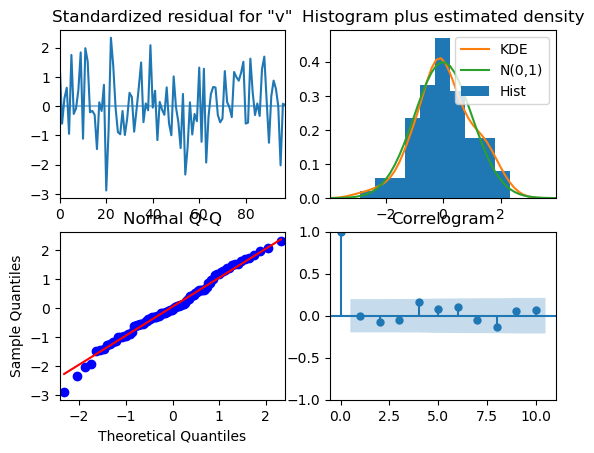

model.plot_diagnostics()